2024 Federal Fall Economic Statement: Highlights and Takeaways

Dec 17, 2024

Under the shadow of the threat of potential 25% tariffs on all exports from Canada heading into the U.S. and with a federal election looming in 2025, the 2024 federal Fall Economic Statement entitled, Reducing Everyday Costs and Raising Wages, arrived at a pivotal moment for the Trudeau government, and for Canada.

This pivotal moment was compounded by the unprecedented circumstances under which the federal Fall Economic Statement (FES) was tabled, including the resignation of Chrystia Freeland, the Deputy Prime Minister and Minister of Finance, just hours before its release. The Hon. Dominic LeBlanc, Minister of Public Safety, Democratic Institutions and Intergovernmental Affairs, has been sworn in as the new Minister of Finance and Intergovernmental Affairs.

While the future of the Trudeau government and the measures contained in the FES are somewhat uncertain, here are the key takeaways for Ontario CPAs based on what was in the document.

Economic Outlook Since Budget 2024

Relative to the April 2024 budget, the government’s economic outlook for this year is more positive, with inflation-adjusted gross domestic product (GDP) expected to grow 1.3%, up from the previous forecast of 0.7%. However, for 2025, the FES expects Canada’s real GDP to grow 1.7%, which is weaker than the 1.9% projected in the April budget.

Despite the stronger economic growth expected this year, the national unemployment rate is projected to be slightly higher in 2024 at 6.4% versus the 6.3% outlined in the April budget. In fact, the unemployment rate is expected to be higher every year over the entire planning period, from 2024 to 2029, signalling a softening labour market.

Inflation—the rate at which consumer prices are increasing—aligns closely with the April 2024 budget and is expected to average 2.1% each year from 2024 to 2028.

Fiscal Developments

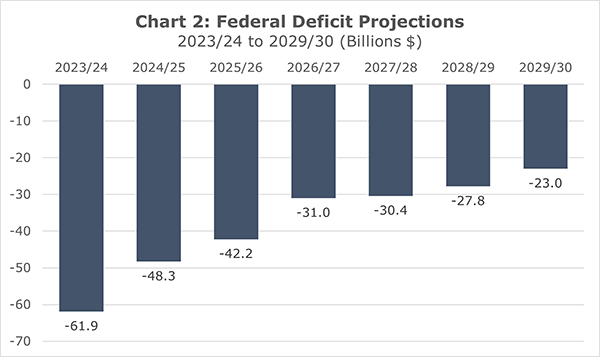

As was anticipated heading into the FES, the government broke through one of its own self-imposed fiscal guardrails from the 2023 FES, which was to not allow the deficit to exceed the $40 billion benchmark.

Looking at the latest numbers for last year (2023/24), the deficit reached $61.9 billion—an increase of nearly $22 billion, or over 50% higher than the $40 billion initially projected. There are many reasons for the changing deficit including lower than expected revenues and the fact the government is now accounting for expense adjustments related to Covid-19 measures ($5.7 billion) and unexpected contingent liabilities ($16.4 billion) that were not previously contained in the April budget.

For the current fiscal year (2024/25), the deficit is also expected to be higher, growing by $8.5 billion to $48.3 billion from $39.8 billion. This is due to revenues being lower than expected, partly because of lower GST revenue from the temporary GST holiday, which has proven to be an administrative challenge for retailers, but also because program spending is now higher by around $6 billion (see Table 1).

Table 1: Fiscal 2024-25—Budget 2024 vs Fall Economic Statement 2024 [Billions $]

|

Total Revenues |

497.8 |

495.2 |

-2.6 |

|

Program Spending |

483.6 |

489.7 |

6.1 |

|

Debt Charges |

54.1 |

53.7 |

-0.4 |

|

Total Spending |

537.7 |

543.4 |

5.7 |

|

Surplus/Deficit |

-39.8 |

-48.3 |

-8.5 |

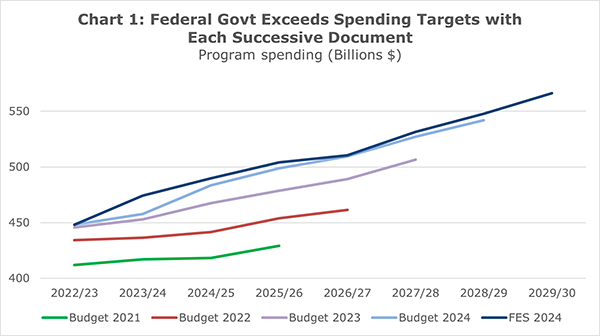

Indeed, the FES continues a longer-term trend from the Trudeau government where it expands spending projections in each subsequent fiscal document (see Chart 1). Consider that, over the period 2023/24 to 2028/29, the FES adds $38.7 billion in cumulative new program spending relative to Budget 2024.

Over the entire fiscal planning horizon in the FES, which includes data up to 2029/30, the government does not plan to balance the budget, meaning deficits as far as the eyes can see (see Chart 2).

Despite higher deficits, the government’s net debt—total liabilities minus financial assets—is projected to maintain a declining trajectory as a share of GDP, falling from 46.1% in 2023/24 to 42.4% in 2028/29.

However, fiscal flexibility concerns arise from uncontrolled spending. Without fiscal prudence, especially during an economic growth cycle, the government reduces its ability to respond to potential unforeseen challenges and diminishes its capacity to enhance Canada's economic competitiveness.

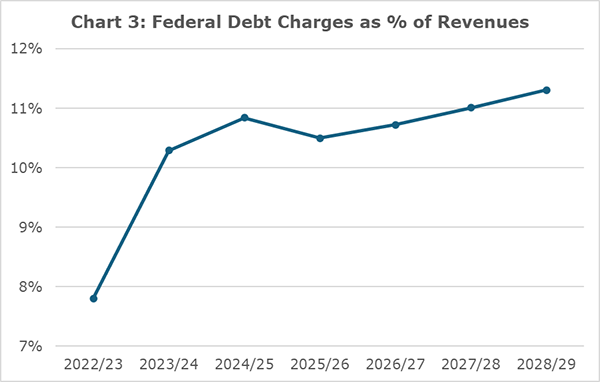

Growing debt charges also pose a concern for fiscal flexibility as they crowd out resources from other public programs and priorities. In the current year, interest on outstanding debt will total $53.7 billion, approximately $14 billion more than Canada’s estimated military spending under NATO definition in 2024/25. When debt charges are considered as a share of total federal revenues, they will reach 11.3% in 2028/29, up from 7.8% as recently as 2022/23 (see Chart 3). Put differently, 11 cents of every revenue dollar collected by the federal government will go to servicing past debt, instead of important public policy initiatives.

Trade, Tariffs, and Taxes

The FES lays out a three-pronged response to U.S. President-Elect Trump’s threat to impose a 25% tariff on all imported Canadian goods and services. The first is further investments in border security and national defence, including an additional $1.3 billion in a border security package to Public Safety Canada, the Canada Border Services Agency, the Communications Security Establishment, and the Royal Canadian Mounted Police.

The second is introducing further trade measures intended to demonstrate the federal government is serious about addressing the incoming U.S. administration’s concerns on trade with China. The FES reiterates a previous announcement on Chinese imports: the imposition of 100% tariffs on all Chinese electric vehicles, a 25% tariff on imports of Chinese steel and aluminum products, and limiting eligibility for federal zero-emission incentives to Canada’s free trade partners.

Building on these previous announcements, the FES also outlines the government’s intention to impose tariffs on imports of certain solar products and critical minerals from China early in the new year, as well as tariffs on semiconductors, permanent magnets, and natural graphite from China beginning in 2026. The FES further proposes legislative amendments to the Export and Import Permits Act that would restrict the importation or exportation of items in response to actions of another country to “create more secure and reliable supply chains.” Additionally, the government will explore the possibility of placing domestic content conditions for federally funded infrastructure projects.

The third prong is introducing measures to boost Canada’s own competitiveness, and the centrepiece here is a proposed tax measure that would reinstate the Accelerated Investment Incentive, which was set to be fully eliminated after 2027. The Accelerated Investment Incentive provides an enhanced first-year capital cost allowance (CCA) for most depreciable capital property. This incentive would apply to qualifying property acquired on or after January 1, 2025, and that becomes available for use before 2030. The FES also proposes to reinstate immediate expensing measures for manufacturing or processing machinery and equipment, clean energy generation and energy conservation equipment, and zero-emission vehicles. The revenue cost of this initiative totals $17.4 billion over five years, and while significant, it will unlikely be enough to attract or retain capital in Canada considering current and future competitiveness challenges.

The FES proposes other, relatively smaller tax measures designed to attract investment and improve Canada’s competitiveness. For instance, the government proposes a capital gains rollover on business investment for small business. Eligible small business shares can be rolled over if the proceeds of disposition are reinvested in other eligible small business shares during the year of disposition or within 120 days following that year. As part of this initiative, the FES proposes to amend the Income Tax Act to expand what qualifies as an eligible small business corporation share and relax certain conditions.

The government also specified the design and implementation details of the EV Supply Chain investment tax credit—a 10% refundable tax credit rate for eligible building property related to three segments of the EV supply chain: EV assembly, EV battery production, and cathode active material production as part of the government’s broader strategy for securing EV production investment.

An additional measure to boost Canada’s competitiveness involves reducing interprovincial trade barriers. The FES indicates an intent to review the Canadian Free Trade Agreement, publish a list of restrictive measures that provinces and territories have in place, and apply conditions on major federal transfers to the elimination of barriers to interprovincial trade and labour mobility.

Innovation and Investment

Improving productivity and jumpstarting innovation is a focus of the FES, and rightly so. Canada is experiencing a productivity “crisis,” as Carolyn Rogers, a CPA and Senior Deputy Governor of the Bank of Canada, noted earlier this year. In fact, recent Statistic Canada data for the third quarter of 2024 marked the ninth quarterly decline in labour productivity in the past 10 quarters.

In response, the FES proposes several new reforms, initiatives, and tax incentives targeted to increase R&D investment and unlock new capital. For starters, it outlines several enhancements to the Scientific Research and Experimental Development (SR&ED) tax credit program that currently supports R&D efforts at over 22,000 businesses in Canada. These changes include raising the annual expenditure cap for Canadian-controlled private corporations to qualify for a 35% investment tax credit from $3 million to $4.5 million; increasing the previous year's taxable capital phase-out thresholds for the enhanced credit from $10 million and $50 million to $15 million and $75 million, respectively; and extending the enhanced refundable SR&ED credit to Canadian public corporations. The proposals would restore eligibility of capital expenditures for both income deductions and the investment tax credit components of the SR&ED program. The cost of the SR&ED enhancements total $1.9 billion over five years, $750 million of which was previously provisioned.

To foster the development and retention of intellectual property in Canada, the FES reveals the government's plan to introduce a patent box regime, expected in Budget 2025.

The FES builds on the government’s AI initiatives. The Business Development Bank of Canada (BDC) will receive $500 million over four years to provide financing and expertise to help small and medium sized businesses adopt digital technologies, focusing on AI. Additionally, $150 million is allocated over three years, beginning in 2024/25, to the Global Innovation Clusters and $24 million over two years, starting in 2025/26, for the National AI Institutes to support AI commercialization.

The FES also proposes significant changes to the rules surrounding pension fund investment. The proposed measures include eliminating the rule restricting Canadian pension funds from owning more than 30% of a Canadian entity’s voting shares. The FES further announces that the government is exploring lowering the 90% threshold that currently limits municipal-owned utility corporations from attracting more than 10% private sector ownership, allowing pension funds to acquire higher ownership shares in these entities.

Additional initiatives to spur investment includes the launching of a fourth round of the Venture Capital Catalyst Initiative with $1 billion in public funding to leverage private venture capital from pension funds and other institutional investors. The government also announced $1 billion in concessional financing (25% of new private investments) to help mid-sized companies get the money they need for long-term growth.

Anti-Money Laundering

The FES proposes several changes around Anti-Money Laundering (AML) and Anti-Terrorist Financing (ATF), likely in preparation for a scheduled mutual evaluation with the Financial Action Task Force (FATF)—an inter-governmental organization dedicated to setting international standards to prevent money laundering and terrorist financing—in December 2025.

The bulk of the measures focus on two areas: 1)“cracking down” on financial crime by addressing and closing existing policy gaps, and 2) empowering existing agencies through stronger penalties and improved inter-agency collaboration.

CPAs should be aware of the largest gaps that the FES aims to close, including the prohibition of anonymous accounts, making reporting to the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC) mandatory, and including company service providers in the AML framework.

There are several other changes focused on FINTRAC, mostly surrounding increasing and expanding penalties for financial crimes, including a proposed new criminal offense for reporting false, misleading, or incomplete information.

The FES proposes a new taskforce for law enforcement and the financial sector, and makes FINTRAC a member of the Financial Institutions Supervisory Committee (FISC). It also proposes launching interdepartmental dialogues with non-profit organizations.

Climate Disclosure

The FES notes the government’s intent to introduce legislative amendments to the Canada Business Corporations Act to create a regulatory authority to enable climate-related financial disclosure requirements for large, federally incorporated privately held corporations. The substance of these changes would be determined through a standard regulatory process and would build on the mandatory climate-related financial disclosures for federally regulated financial institutions and federal Crown corporations.

In Conclusion

Notably missing from the FES is the $250 “Working Canadians Rebate,” a proposed tax rebate targeted at working Canadians who earned up to $150,000 in 2023. Its absence speaks to the ongoing political uncertainty, the departure of the former Minister of Finance, and the future of the government as it continues to rely on the NDP and the Bloc to support its minority status.

With approximately a month until the inauguration of President Trump, Reducing Everyday Costs and Raising Wages was introduced at a time of great uncertainty, both on the domestic political scene and in relation to developments with our largest trading partner. The FES signals how the government plans to respond to the challenges from south of the border, and the challenges here at home.