Trump’s Tariff Turmoil – Insights from CPAs

February 6, 2025

Editor’s note: As the Trump administration's sweeping tariffs create waves in the economic landscape, the role of Chartered Professional Accountants (CPAs) is more pivotal than ever. CPAs are essential in helping businesses navigate the complex and rapidly changing trade environment. CPA Ontario will continue to bring strategic insights to members to help them navigate the challenges ahead.

What a whirlwind this past week has been. Let’s get caught up and then dive into the perspective of three expert CPAs on the evolving tariff threats.

What Happened and How We Got Here

On February 1, 2025, the Trump administration shook the economic landscape by announcing a set of sweeping tariffs through an Executive Order set to take effect on February 4, 2025. The mandate included a hefty 25% tariff on most Canadian imports, a similar 25% on Mexican imports, and an additional 10% tariff on imports from China. Energy resources from Canada, including oil, gas, and electricity, were not spared, but faced a lower tariff rate of 10%. As motivation, Trump cited a national emergency related to illegal immigration and drug trafficking across borders.

In swift response, the Canadian government, led by Prime Minister Justin Trudeau, unveiled a package of retaliatory measures, including a 25% tariff on $155 billion in goods imported from the United States, starting with $30 billion in goods on February 4. Premiers committed to a series of their own measures, such as pulling U.S. alcohol from shelves, to inflict economic pain on our southern neighbor.

On February 3, a day before the tariffs would take effect, a deal was reached between President Trump and Prime Minister Trudeau to postpone the tariffs for 30 days. In an X post delivering the news, Trudeau wrote:

I just had a good call with President Trump. Canada is implementing our $1.3 billion border plan — reinforcing the border with new choppers, technology and personnel, enhanced coordination with our American partners, and increased resources to stop the flow of fentanyl. Nearly 10,000 frontline personnel are and will be working on protecting the border. In addition, Canada is making new commitments to appoint a Fentanyl Czar, we will list cartels as terrorists, ensure 24/7 eyes on the border, launch a Canada- U.S. Joint Strike Force to combat organized crime, fentanyl and money laundering. I have also signed a new intelligence directive on organized crime and fentanyl and we will be backing it with $200 million. Proposed tariffs will be paused for at least 30 days while we work together.

Trump posted something similar on Truth Social, noting in the end that:

I am very pleased with this initial outcome, and the Tariffs announced on Saturday will be paused for a 30 day period to see whether or not a final Economic deal with Canada can be structured.

Take a moment to catch your breath; that last comment from Trump about finalizing an economic deal is key.

While a postponement is welcome, there continues to be uncertainty over the trade relationship between the two nations. In fact, for some time now, the threat of tariffs on Canadian imports to the U.S. has been a cloud over the Canadian economy, imposing immense uncertainty, going back to Trump’s now infamous Truth Social post in November 2024. Ever since, the question we have all grappled with for months was whether Trump would or would not impose tariffs on Canadian products entering the U.S.

Trump’s penchant for tariffs is no secret. Throughout his campaign and presidency, he has frequently articulated his desire to impose higher duties on countries like Mexico and China.

If there’s a silver lining to the roller coaster of the past week, it’s that we have more information. We now know what the President’s tariff plan is, along with the federal and provincial governments’ proposed retaliation.

It is against this backdrop of economic tension and political maneuvering that CPAs find themselves at a critical juncture. The role of CPAs is more pivotal than ever, as businesses navigate the rough waters of international trade, manage the risks associated with tariffs, and provide strategic counsel to businesses impacted by these sweeping changes.

What Does This Mean for Ontario CPAs

For CPAs in Ontario, the unfolding tariff saga translates into an immediate need for strategic adjustments. Increased tariffs would undoubtedly affect the bottom line of businesses dependent on cross-border trade, and lead to downstream impacts on Canada’s economy. To dig into what CPAs should consider over the next 30 days and beyond, we spoke to three CPAs – Babar Khan, Paul Tyers and Haroon Khan. With over 45 years of combined cross-border expertise, these CPAs shared their thoughts on how they are approaching the tariff threat, where they’re seeing impacts, and what they’re hearing in the field.

Cross-Border Trade: The Short and Long-Term Impacts

It’s well known that there is a deep economic link between Canada and the U.S. - 77% of Canadian exports go to the U.S., while Canada is the top export market for 34 states. Add to this the complexity of supply chains between the two countries – for example, auto parts may cross the U.S.- Canadian-Mexico borders up to eight times before final assembly – and it becomes clear why changes in tariffs and trade policies can have widespread effects on the Canadian economy.

This is even before you consider the downstream impacts; services supporting these industries will also see knock on effects. As Haroon Khan, a seasoned Canadian and U.S. tax professional with over 14 years of experience at top accounting firms, put it: “...everybody knows about the ripple effect that we’re going to have on the whole economy.”

In its latest Monetary Policy Report, released before Trump’s Executive Order, the Bank of Canada explored a more severe scenario than current tariff plans, assuming a 25% tariff on all trading partners and products. Despite its severity, this scenario gives a sense of the potential economic damage: a 2.5% drop in GDP in the first year, compared to a no-tariff situation.

In the days after the Executive Order announcement, Trevor Tombe, University of Calgary economics professor, estimated the employment impact of the tariffs, noting that Canada could see 600,000 fewer jobs, with the unemployment rate reaching 10%.

The economic effects should be a “wake up call” for Canada, Haroon said.

Inflationary impacts are also worth considering; tariffs will lead to increased costs for businesses, which would then be passed on to consumers (to what extent, we aren’t sure), reducing purchasing power.

Despite the fluidity of the situation, all three CPAs outlined both short-term and long-term considerations for addressing tariffs. In the short term, Babar Khan, a cross-border tax expert with over 14 years of experience, and an Adjunct Professor at the Schulich School of Business, suggested that businesses could use the next 30 days to mitigate impacts by front-loading goods shipments to the U.S., buying extra time while the situation shakes out. In the longer term, all three CPAs agreed that diversifying trade relationships and supply chains is crucial – for example, Babar emphasized that Canada already has 15 free trade agreements and these are a start for reducing reliance on the U.S.

Uncertainty and Risk Management

One thing to keep in mind is that tariffs don’t need to be enacted to dampen economic activity in Canada; the threat alone can result in economic disruption.

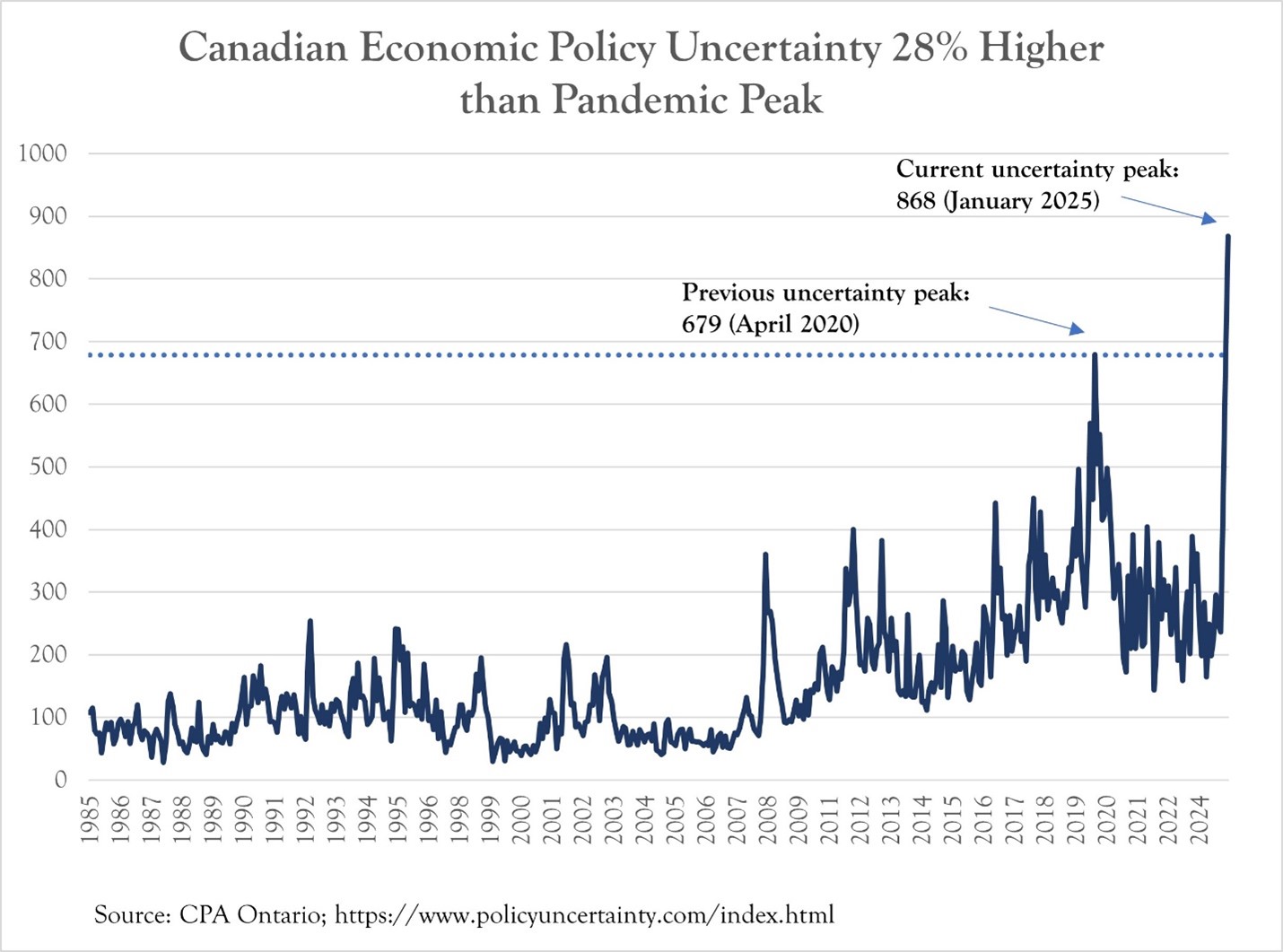

To help contextualize the level of economic policy uncertainty in Canada; data from the Economic Policy Uncertainty Index shows that Canada is experiencing an unprecedented level of uncertainty – in fact, it is 28% higher than the previous peak observed during the COVID pandemic.

Paul Tyers, FCPA, FCA, Managing Director and Portfolio Manager at Wealth Stewards Inc. emphasized that uncertainty can lead to deferred business decisions: “it will lead to delayed decisions on capital expenditures, and delayed decisions about hiring.” He shared an example of a bakery in his portfolio that is experiencing delays in scaling up due to the threat of tariffs.

Babar likened uncertainty to an “invisible tax,” and highlighted that he believes certainty is what differentiates developed economies from developing ones. “Businesses don’t like uncertainty, bureaucracy, or complexity.” Unfortunately, this tariff situation taps into all three.

In an environment of trade wars and tariffs, there is a risk that the Canadian dollar could slide in relation to its U.S. counterpart. Haroon has observed that some companies have already started using foreign exchange hedging contracts to manage this risk. "I know some public corporations, ... they have already anticipated that some of these things will happen, and they started to go towards foreign exchange hedging contracts because they know one of the things that will happen very soon is the fluctuation in the Canadian exchange rate.”

Babar expressed that continued devaluation of the Canadian dollar has both upsides and downsides. On the one hand, a lower dollar can cushion some of the blow of U.S. tariffs by making Canadian exports relatively more attractive at a lower price. However, this benefit is contextual. Some businesses that purchase products and inputs from abroad will have to pay more with a lower Canadian dollar.

Another risk management consideration in this environment is transfer pricing, which is the practice of setting prices for transactions between different parts of the same company to manage tax liabilities across different countries. In Babar’s view, the need for optimization of transfer-pricing arrangements would be more pronounced if the tariffs are 1) actually implemented and 2) durable over the long term. And there is reason to doubt both. The 30-day tariff reprieve casts hopeful doubt on implementation. And Babar believes Congress buy-in and political pressure from bordering U.S. states could lessen the durability of tariffs.

When it comes to tax planning, CPAs should be mindful of opportunities given the tariff situation and the fact that the Trump administration might follow through with further tax cuts, namely to the U.S. corporate income tax rate. Both forces would make Canadian production and profitability less attractive. This should be monitored closely.

Opportunities for CPAs

Difficult times like the current moment present an opportunity for CPAs to provide important value to their clients. The temporary reprieve of a 30-day delay offers a window for CPAs and businesses to prepare and strategize, but this period is fraught with uncertainty as both nations work towards a possible economic deal – if this is indeed what President Trump’s endgame is. The outcome of these negotiations will shape the economic landscape for years to come, making the role of the CPA more critical than ever as trusted advisors in turbulent times.

Paul noted that private businesses may not have access to an internal economist or a Chief Financial Officer, making CPA guidance invaluable. Haroon emphasized the crucial role CPAs can play in advising businesses on navigating changing trade policies and tariffs, including diversifying suppliers and optimizing supply chains.

For CPAs serving in an advisory or strategic capacity, all three CPAs stated that it is essential to proactively reach out to clients, advise on developments in the environment, discuss their situations, and provide guidance on strategies to mitigate the effects of tariffs. Paul thinks: “this uncertainty is an opportunity for CPAs... I would be proactive and be on the phone and say how can we assist you with this uncertainty.”

In conclusion, Trump’s tariffs are more than just a headline – they are a clarion call for CPAs to engage deeply with the implications for international trade, economic stability, and client advisement. As we navigate this complex terrain, the expertise and proactive strategies of CPAs will be indispensable in steering businesses through the challenges and opportunities that lie ahead.

Bios

Babar Khan is an experienced cross-border tax professional with over 15 years of experience in US & Canadian tax compliance and advisory work. Babar holds an MSc (Tax) from University of Oxford (UK), an MBA from Schulich School of Business and a BBA from University of Toronto.

Haroon Khan is an experienced tax professional with over 14 years of service at the world's leading accounting firms. Haroon earned a Bachelor of Business Administration degree from the University of Toronto before qualifying as a CPA, CA in Canada and a US CPA in the state of Illinois.

Paul Tyers FCPA, FCA, CFP®, CIM Managing Director and Portfolio Manager Wealth Stewards Inc. a pioneer in Canada for helping pave the way for CPA’s to Integrate Wealth Management into their practices. Paul is internationally recognized in the finance industry. Wealth Stewards held a webinar called Outlook 2025 which touched on some of these topics as well as other economic trends in 2025 – watch here.